Caixabank (Go to Home)

Caixabank (Go to Home)

Print page

Print page

26 October 2014

|

min read

CORPORATE

Cataluña

BARCELONA

la Caixa Group passes the ECB Comprehensive Assessment with a CET1 ratio of 9.3% under the adverse scenario, while CaixaBank would achieve 10.3%

la Caixa Group passes the ECB Comprehensive Assessment with a CET1 ratio of 9.3% under the adverse scenario, while CaixaBank would achieve 10.3%

la Caixa Group passes the ECB Comprehensive Assessment with a CET1 ratio of 9.3% under the adverse scenario, while CaixaBank would achieve 10.3%

Outcomes comfortably exceed minimum capital requirements set at 5.5%

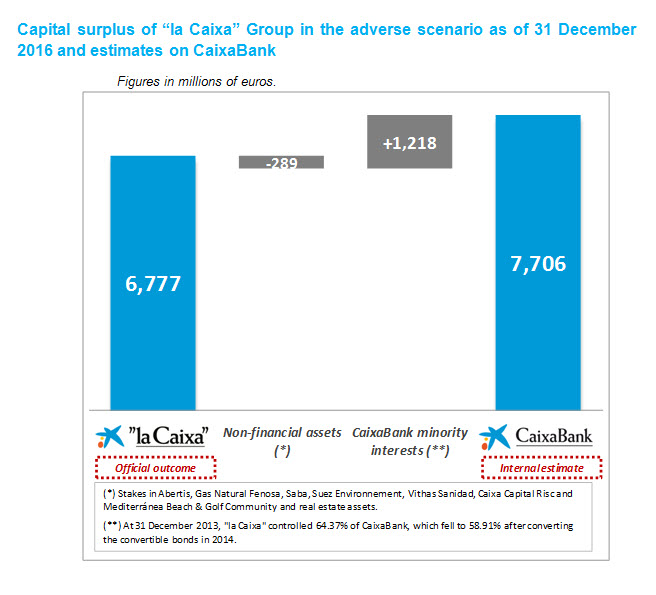

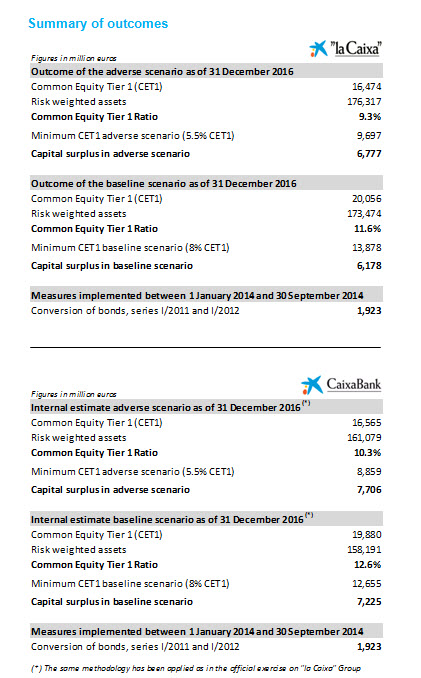

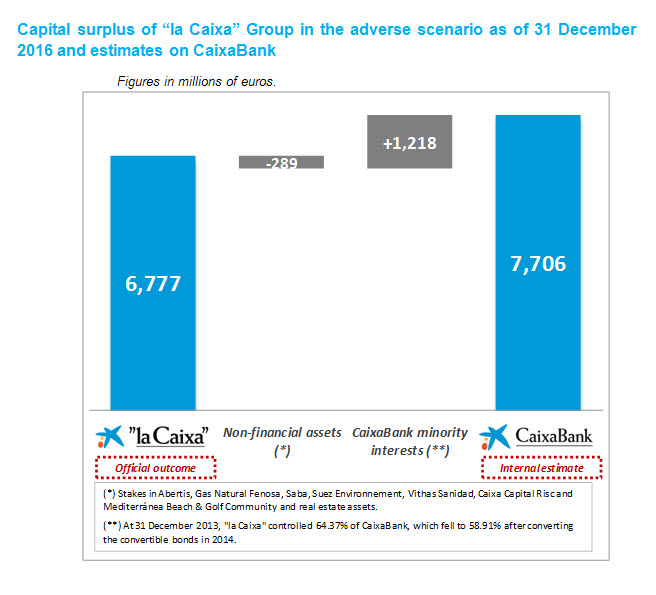

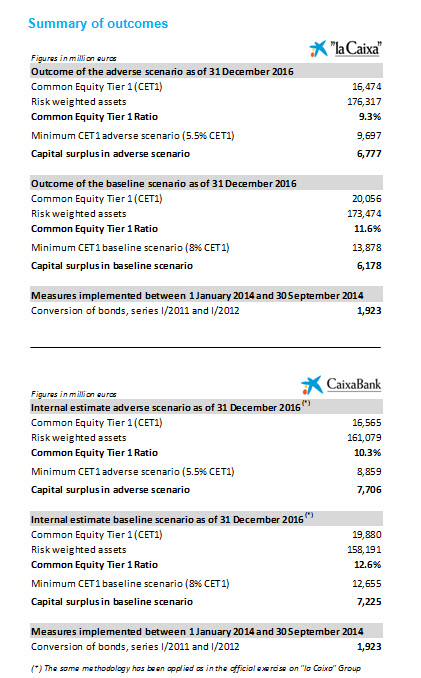

- "la Caixa" Group, which includes CaixaBank, as well as the industrial and real estate assets of Criteria CaixaHolding, has a capital surplus of 6.8 billion euros under the adverse scenario, while CaixaBank would achieve a surplus of 7.7 billion euros.

- Isidro Fainé, Chairman of "la Caixa" Group, believes that these outcomes confirm "our excellent financial strength, even under the adverse scenario, thanks to prudent management, which has enabled us to reach high solvency levels and boost organic and inorganic growth".

- Taking into account the conversion of mandatory convertible bonds during the first half of 2014, CaixaBank's CET1 ratio would, according to internal estimates, stand at 11.4% under the adverse scenario, more than doubling the minimum level required, with a surplus of close to 9.5 billion euros.

"la Caixa" Group, which includes CaixaBank as well as the industrial stakes and real estate assets of Criteria CaixaHolding, has comfortably passed the Comprehensive Assessment conducted by the European Central Bank, that consists of a detailed asset quality review (AQR) and a strict stress test coordinated by the European Banking Authority (EBA).

The stress test methodology under the adverse macroeconomic scenario has been applied to CaixaBank in an internal exercise, resulting in a capital surplus of 7.7 billion euros and a Common Equity Tier 1 (CET1) ratio of 10.3%. CaixaBank, the leading Spanish financial institution, reports a greater capital position than "la Caixa" Group mainly due to a limitation on the contribution from the bank's minority interests and the capital impact of the non-financial stakes held by Criteria CaixaHolding, a subsidiary of "la Caixa" Group.

The European authorities have taken into account the whole of "la Caixa" Group, including the industrial stakes and real estate assets of Criteria CaixaHolding, based on the highest consolidation level as of 31st December, 2013 in Caja de Ahorros y Pensiones de Barcelona, which became a banking foundation in 2014. As a result, "la Caixa" Group achieves a capital surplus of 6.8 billion euros under the adverse scenario, with a Common Equity Tier 1 (CET1) ratio of 9.3%.

The AQR confirms the bank's high NPL coverage

The Asset Quality Review (AQR) involved a thorough analysis of the asset quality of certain portfolios selected by the supervisory authorities (SMEs, corporates, large corporate, real estate developers and real estate assets), representing more than 52,000 million euros of credit risk-weighted assets of "la Caixa" Group, well above 50% of the total amount. This assessment was carried out on both a collective and individual basis. The latter consisted of specific reviews of 935 borrowers, selected either by size or randomly and implied the analysis of more than 18,000 contracts as well as the reappraisal of more than 7,100 collaterals.

This thorough review concluded that additional provisioning requirements were almost negligible, confirming a high NPL coverage and the bank's prudent approach to recognising and setting aside provisions for impaired assets.

A sound position from which to face future challenges

According to Isidro Fainé, Chairman of "la Caixa" Group, the ECB comprehensive assessment has confirmed "our excellent financial strength, even under worst-case scenarios, thanks to prudent management, which has enabled us to reach high solvency levels and boost organic and inorganic growth".

Gonzalo Gortázar, CaixaBank's CEO, added that "these results reaffirm CaixaBank's presence among those institutions that do not require additional capital in any of the assessed scenarios, and will enable us to comfortably face the future challenges to be included in our forthcoming 2015-2018 Strategic Plan, which aims to reinforce our leadership and improve profitability".

According to internal estimates, and taking into account the conversion of 1.9 billion euro of mandatory convertible bonds during the first half of 2014, CaixaBank's CET1 ratio would be 11.4% under the adverse scenario, more than double the required minimum, with a surplus of around 9.5 billion euros. Even under a "fully-loaded" Basel III framework, CaixaBank would still report a CET1 ratio of 10.4% under the adverse scenario.

This result is also a reflection of CaixaBank's leading capital position at the end of the third quarter of 2014, with a CET1 capital ratio of 13.1% (12.7% fully loaded), as well as of the Banks's high and prudent provisioning level, the strength of its operating profit, and the credit quality of its loan portfolio.

{kind=link}

{kind=link}