Caixabank (Go to Home)

Caixabank (Go to Home)

Print page

Print page

30 April 2025, 00:00h

|

min read

CORPORATE

REGULATORY

National

BARCELONA

CaixaBank earns €1.47 billion in the first quarter, up 6.9% in comparable terms

Gonzalo Gortázar, CaixaBank’s CEO, during the 1Q25 Results presentation

Gonzalo Gortázar, CaixaBank’s CEO, during the 1Q25 Results presentation

- Gonzalo Gortázar, CaixaBank’s CEO, said that “we have started the first year of our new Strategic Plan with remarkable progress towards our goals: we’re accelerating business growth; driving transformation and investment in the business; and we’ve reduced non-performing loans while maintaining high levels of liquidity and capital”.

- Gortázar reinforced that “our great results will allow us to continue supporting families and companies, as well as the economy and society, a mission that is even more necessary in an environment of growing uncertainty like the one we currently face”.

- Driving economic activity. The bank has made a strong start to its new 2025–2027 Strategic Plan, reporting an 8.5% increase in customer funds and a 2.9% rise in performing loans compared to March 2024. The bank has also gained nearly 340,000 new customers in Spain over the past 12 months.

- New lending performed well during the period, especially mortgages, which are up 62% compared to the first quarter of 2024 to reach €4.51 billion, and consumer lending, which rises 11% to €3.37 billion.

- Wealth management balances are up €18.41 billion compared to March 2024 (+7.5%) to €264.4 billion, supported by net subscriptions of mutual funds and savings insurance.

- Profit is 6.9% higher on a like-for-like basis. Accounting profit climbs 46.2%, after recording 25% of the banking tax on NII and Fees on a linear accrual. This represented €148 million for the first quarter of 2025, whereas in 2024 the entire year’s tax levied on the bank for a total of €493 million was recorded in the first quarter. Notably, quarterly profit would have been 6.9% higher had the tax been allocated evenly throughout 2024 (at a rate of €123 million per quarter).

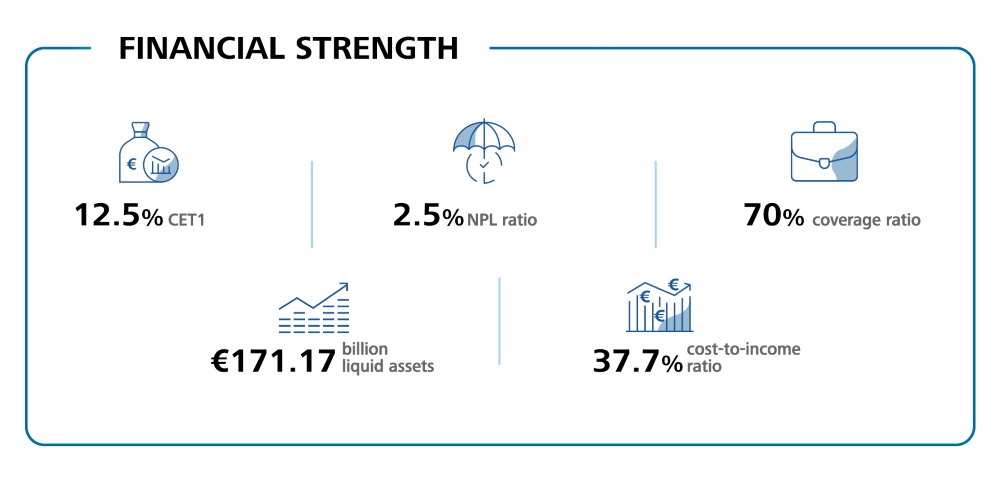

- The NPL ratio falls to reach all-time low levels of 2.5% (2.6% at the end of 2024), while the coverage ratio is 70%.

- The Group boasts a comfortable liquidity and capital position. Total liquid assets amount to €171.17 billion, while the CET1 ratio comes to 12.5%.

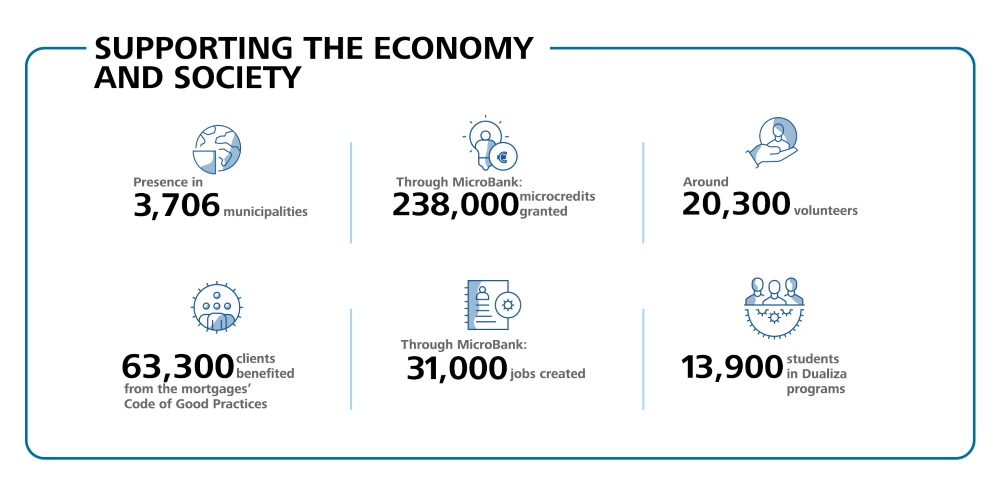

- Ongoing support for the economy and society. In rolling out its new strategic plan, CaixaBank remains true to its essence by embracing a different way of banking that fosters social and financial inclusion: the bank is present in 3,706 municipalities; has more than 360,000 customers with basic payment accounts, and around 20,300 volunteers who have taken part in some 29,100 activities over the last 12 months.

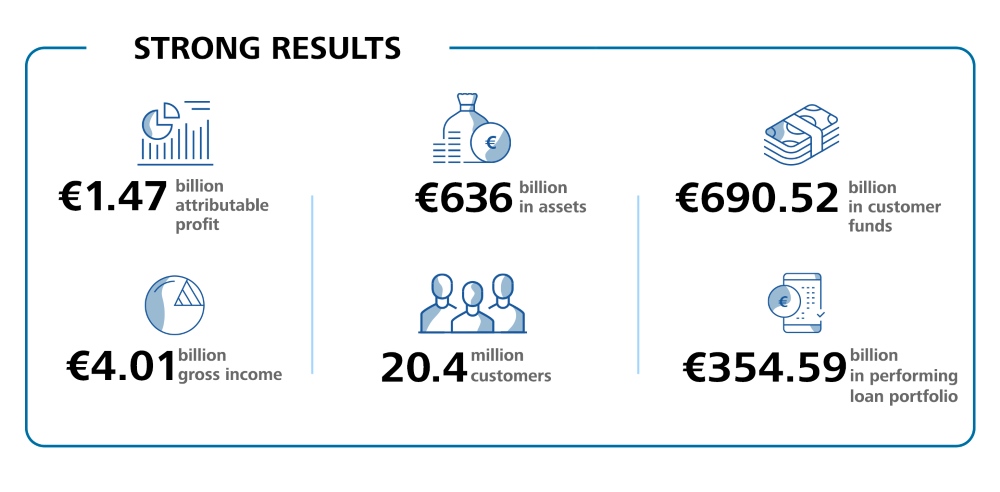

The CaixaBank Group, which serves 20.4 million customers through a network of more than 4,100 branches across Spain and Portugal, posted a net attributable profit of €1.47 billion in the first quarter of the year, compared to €1.01 billion in the same period of 2024 (up 46.2% and 6.9% on a like-for-like basis).

CaixaBank’s Chief Executive Officer, Gonzalo Gortázar, remarked that “we have started the first year of our new Strategic Plan with remarkable progress towards our goals: we’re accelerating business growth; driving transformation and investment in the business; and we’ve reduced non-performing loans while maintaining high levels of liquidity and capital”.

In this context, Gortázar reinforced that “our great results will allow us to continue supporting families and companies, as well as the economy and society, a mission that is even more necessary in an environment of growing uncertainty like the one we currently face”.

Ramping up growth and transformation

In November 2024, CaixaBank unveiled its new 2025–2027 Strategic Plan, with the aim of maintaining sustainable profitability levels through three strategic pillars: ramping up growth, driving business transformation and investment, and consolidating the company’s position as a market leader in sustainability.

The company has begun to roll out its new strategic plan, focused on ramping up growth and transforming and investing in the business.

The positive commercial momentum continued throughout the first quarter: business volume once again exceeded €1 trillion, with the customer base in Spain growing by nearly 340,000 in the past 12 months to reach 18.6 million customers, of whom 71.5% hold at least three products with the bank. Digital customers are also on the rise, exceeding 12.2 million in March 2025, more than half a million more than a year ago.

In terms of the transformation process, CaixaBank continues to leverage technology to enhance its commercial capabilities and customer experience and is already embracing new technologies and developing new capabilities in the day-to-day running of the business.

In this context, CaixaBank Tech, CaixaBank's technology subsidiary, has strengthened its workforce by adding almost half of the Group’s approximately 1,250 new net hirings in the last year, of which nearly 400 are developers.

Customer funds are up 8.5% and the performing loan portfolio rises 2.9% compared with the first quarter of 2024

The results obtained in the first quarter of 2025 also reflect the strength of CaixaBank’s business and the strong growth in commercial activity. The bank has made a strong start to its new 2025–2027 Strategic Plan, with a 2.9% increase in the performing loan portfolio and an 8.5% increase in customer funds compared with March 2024.

Gross customer lending stood at €364.16 billion on 31 March 2025. The performing loan portfolio amounted to €354.59 billion, up 2.9% on March 2024 (+0.9% in the quarter), with positive contributions from lending to companies and individuals, on the back of higher demand and higher loan production.

With new loan origination faring well across all retail segments in Spain, ending the period at €18.88 billion (+15%), new mortgage production stood at €4.51 billion in the first quarter of 2025, up 62% year on year, with around 93% of the total arranged at a fixed rate. Meanwhile, a total of €3.37 billion was granted in consumer loans, up 11%; while lending to companies increased by 4% to reach €10.99 billion.

Customer funds totalled €690.52 billion, having risen by €54.03 billion (+8.5%) in the last 12 months (€5.16 billion in the quarter, +0.8%). Wealth management balances were up €18.41 billion on March 2024 (+7.5%) to €264.4 billion, supported by net subscriptions in mutual funds and savings insurance, and despite a decline in pension plans in the quarter, mainly due to unfavourable market conditions.

CaixaBank maintained its market share leadership in wealth management by claiming 29.2% of the market, widening the gap with its competitors.

Profits rise 6.9% on a like-for-like basis

Profit amounted to €1.47 billion, up 46.2% in the quarter. Notably, the entire year’s tax levied on the bank was recorded in the first quarter of 2024, for a total of €493 million. However, only 25% of the tax on net interest and fee and commission income was recognised in this first quarter of 2025, representing €148 million. This difference goes some way to explaining the growth in earnings for the quarter, which would have grown by 6.9% had the tax been accounted on a linear accrual basis throughout 2024 (on the basis of €123 million per quarter).

The income statement reflects the decline in market interest rates, with a 4.9% drop in net interest income to €2.65 billion, partially offset by growth in volumes. The customer spread narrowed by 11 basis points in the quarter to 3.20%.

Meanwhile, revenue from services (wealth management, protection insurance and bank fees) increased by 6.8%. Income earned from wealth management grew by 16.5% compared with the same period of 2024 due to sustained volume growth and intensive commercial activity; income from protection insurance was up 1.9%; and banking fees income also performed well (+1.4%), although recurring banking fees dipped by 1.4%.

Looking at dividend income, the year-on-year change was largely due to the dividend received from BFA (€50 million in the first quarter of 2025), while in 2024 it was recorded in the second quarter (€45 million). Attributable profit from entities accounted for using the equity method amounted to €72 million, up 27.7% year on year.

The new accounting treatment of the tax on interest and fee and commission income – in 2024, the entire tax on banks was recognised under ‘Other operating income and expenses’ but is now recorded on a straight-line basis under ‘Income tax’ – has also affected the performance of margins, profitability and cost-to-income.

The growth in gross income, up 14.7% year on year (to €4.01 billion), outpaced the growth in recurring administrative expenses, depreciation, and amortisation (+4.8% to €1.58 billion), enabling operating income to grow to €2.43 billion at quarter-end (+22.3%). Meanwhile, the cost-to-income ratio stood at 37.7%.

In terms of profitability, ROE climbed to 16.5% (15.4% assuming the straight-line accrual of the banking tax on NII and Fees), compared to 13.4% in March 2024.

Financial strength and an NPL ratio at all-time low levels

The CaixaBank Group continues to bolster its financial position, with an NPL ratio that remains well contained and at historically low levels, coupled with a comfortable liquidity position and strong organic capital generation.

The balance of non-performing loans fell for yet another quarter (-€160 million) to end the period at €10.08 billion, thanks to active risk management, with an NPL ratio of 2.5% (2.6% at year-end 2024) and a coverage ratio of 70%. The cost of risk also receded, falling to 0.25% (last 12 months).

CaixaBank also has a comfortable liquidity position, with total liquid assets amounting to €171.17 billion. The Liquidity Coverage Ratio (LCR) was 197% on 31 March, well in excess of the minimum requirement of 100%.

The Group boasts a strong capital position, with a Common Equity Tier 1 (CET1) ratio of 12.5% at the end of the quarter. This ratio reflects an extraordinary impact of +20 basis points (bps) following the entry into force of the CRR3 (Basel IV) regulations in January 2025. The change in the CET1 ratio in the first quarter, excluding the extraordinary impact of Basel IV, was a positive 7 basis points and is largely due to organic growth (+51 bps), less the forecast dividend charged to earnings for the year (60% payout) and payment of the AT1 coupon (-40 bps), as well as the performance of the markets and other factors (-4 bps).

The current 2025–2027 Strategic Plan sets an internal CET1 target ratio of between 11.5% and 12.5%, with an interim target of between 11.5% and 12.25% for 2025. The upper limit of the target sets the threshold for possible extraordinary capital distributions. On 31 March, the regulatory CET1 ratio was 12.25%, after deducting the excess capital above the upper limit of the target set for 2025.

Ongoing support for the economy and society

At the start of the deployment of its new strategic plan, CaixaBank has remained true to its essence by embracing a different way of banking and providing ongoing support for families, businesses and society at large through initiatives related to financial inclusion, solutions with a social impact, social projects across the land, and a firm commitment to the environment.

In terms of promoting financial inclusion, the bank is present in 3,706 municipalities across all of Spain with a physical branch, ATM or mobile branch, meaning that it succeeded in adding a further 564 municipalities in the last 12 months.

CaixaBank also has more than 360,000 customers with basic payment accounts and around 20,300 volunteers who have taken part in some 29,100 activities over the last 12 months.

Meanwhile, MicroBank, Europe’s leading microcredit institution, has continued to promote financing with a positive social impact. In the past 12 months, MicroBank has granted more than 238,000 microloans and helped to create more than 31,000 jobs. In the realm of education, more than 13,900 students benefited from CaixaBank’s Dualiza programmes to promote dual vocational training.

Since the Euribor moved back into positive territory, the bank has facilitated payment agreements for loans, debt refinancings or solutions linked to the Code of Good Mortgage Practices, benefiting more than 63,300 customers.

Video CaixaBank's CEO, Gonzalo Gortázar

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}