Caixabank (Go to Home)

Caixabank (Go to Home)

Print page

Print page

28 October 2022

|

min read

CORPORATE

Comunidad Valenciana

VALENCIA

CaixaBank earns €2.46 billion through to September, up 17.7% on a like-for-like basis, following activity growth and cost savings arising from the integration

Image of Gonzalo Gortazar at CaixaBank at the first nine months of the year results press conference.

Image of Gonzalo Gortazar at CaixaBank at the first nine months of the year results press conference.

- Attributable profit falls by 48.8%, due to extraordinary accounting impacts arisen from the Bankia integration.

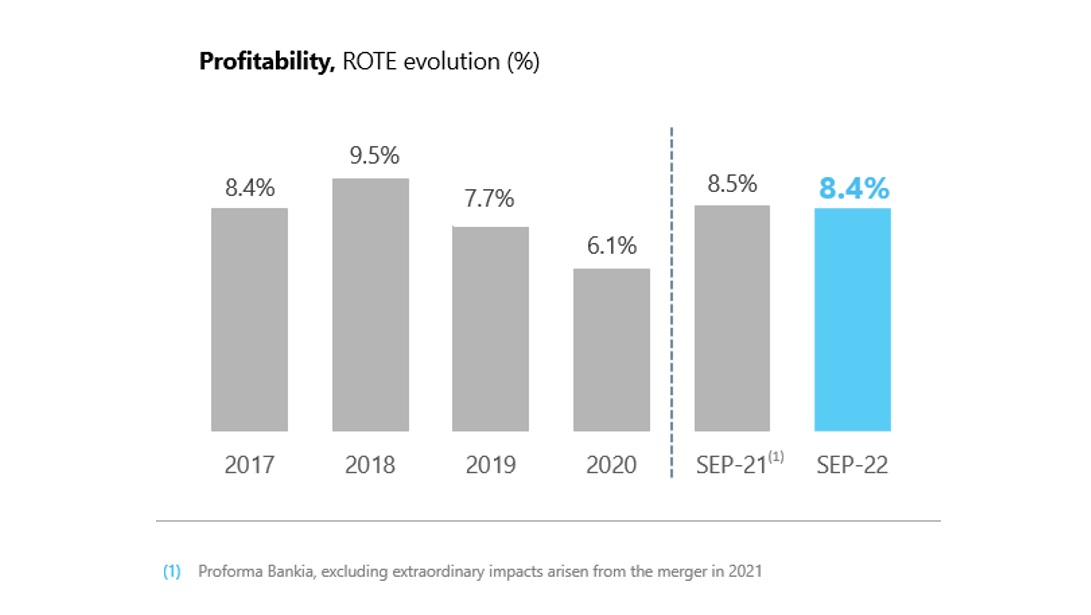

- Profitability ratios stay in line with those of 2021. ROTE stands at 8.4%, still below the cost of capital.

- Performing loans grow by €11.49 billion to reach €351.46 billion, with a sharp increase in new production. The performing business-loan portfolio gains 7% in the year to date, while the performing consumer lending portfolio climbs by 3.6% and the performing mortgage portfolio, by 0.8%.

- Customer funds total €612.5 billion. Despite the difficult macroeconomic environment and adverse market conditions, highlights in the period include net inflows of €10.95 billion, leading to significant increases in market shares in mutual funds, pension plans and savings insurance.

- The bank continues to generate cost synergies. In the first nine months of the year, it achieves a 5.9% reduction in recurring administrative, depreciation and amortisation expenses, due to the savings arising from the merger.

- Gonzalo Gortazar, CEO of CaixaBank, highlights that “we now face the next quarter from a position of financial strength, thus allowing us to help society amid the current uncertain climate, as stated in our new brand purpose: ‘Standing by people for everything that matters’”.

- In the last seven years, 72% of the residential mortgage portfolio has been originated at fixed rates and this figure has risen to over 90% in the first nine months of this year.

- The NPL ratio continues to decline and now stands at 3%, a level not seen since 2008. Meanwhile, the coverage ratio improves by five percentage points to 68%.

- Strong capital position and liquidity. The CET1 capital ratio reaches 12.4% and total liquid assets amount to €141.98 billion.

- Financial inclusion and solutions for vulnerable groups. CaixaBank is physically present in more than 2,200 municipalities and is the only bank in 470 of them, while a further 626 have their banking needs covered by a mobile branch (the “ofimóvil” branch in a bus). Moreover, 357,000 customers have a commission-free social account. In the last ten years, CaixaBank has signed the 35% of the total contracts in the sector abiding by the Mortgage Code of Best Practices.

The CaixaBank Group posted an attributable net profit of €2.46 billion in the first nine months of the year, up 17.7%, on a like-for-like basis, on the same period of the previous year. This growth has been driven by strong commercial activity and cost savings achieved thanks to the synergies arising from the merger. Profitability ratios stay in line with those of 2021. Profitability (ROTE) was 8.4%, still below the cost of capital.

Reported profit increased 21.5%, excluding the extraordinary effects arisen from the merger. If the impacts of the merger are taken into account, profit is down 48.8% year-on-year as the figure at 30 September 2021 was €4.80 billion, due to the positive contribution for accounting purposes of €4.3 billion in badwill and other extraordinary items associated with the merger.

Gonzalo Gortazar, CEO of CaixaBank, highlighted that “in a year marked by the completion of the integration, the bank has once again demonstrated its commercial strength, which together with the synergies arising from the Bankia integration, has allowed us to increase our profit by 17.7% on a like-for-like basis”.

Gortazar also praised the performance of the business and remarked that "when it comes to customer funds we have attracted almost €11 billion in net inflows across savings insurance, asset management and deposits, despite market volatility”. “It is this dynamism of the long-term savings segment and protection insurance that has boosted our revenues, although net interest income was still slightly down", underlined the bank’s CEO.

He added that “we now face the next quarter from a position of strength, thus allowing us to help society amid the current uncertain climate, as stated in our new brand purpose: ‘Standing by people for everything that matters’”.

Income statement (on a like-for-like basis)

Earnings for the first nine months of the year, which are comparable with the pro-forma results of Bankia and CaixaBank in the same period of the previous year, excluding the extraordinary items arising from the merger, highlight solid revenues reaching €8.65 billion, up 2.7% on the same period of the previous year. The decline in net interest income (-0.4%) and revenues from stakes (-34.7%) are offset by the positive performance of the rest of revenues (+6.9%), following a strong commercial activity.

In addition, gross income growth (+2.7%) and a reduction in recurring administrative, depreciation and amortisation expenses (-5.9%) generated significant growth in pre-impairment income excluding extraordinary items (+14%).

Dividends totalled €132 million between January and September and included, in the second quarter, dividends paid by Telefónica and BFA amounting to €38 million and €87 million, respectively (€51 million and €98 million in 2021).

Meanwhile, equity-accounted attributable earnings came to €207 million. The year-on-year change (-43.5%) was due to the bank's divestment of its stake in Erste Group Bank and the full consolidation of Bankia Vida since January 2022, among other factors.

Recurring banking fees and commissions were up 2.1% year-on-year, largely due to higher transactional activity and growth in payments, which offset the impact of the unification of CaixaBank and Bankia's customer loyalty programmes.

When it comes to costs, CaixaBank successfully reduced recurring administrative, depreciation and amortisation expenses (-5.9% year-on-year) in the first nine months of 2022, thanks to the synergies arising from the merger with Bankia. More precisely, personnel expenses were down 8.5%, due to the savings achieved following the departure of employees under the Labour Agreement framework, while general expenses fell by 6.6% thanks to the synergies achieved.

Consolidation of commercial activity in customer lending

The year has seen growth in lending to both retail and business customers, with the performing loan portfolio (excluding NPLs) growing by €11.49 billion (+3.4% in the year) to reach €351.46 billion. In particular, the performing business lending portfolio has grown 7%, while the performing consumer lending and mortgage portfolios have risen by 3.6% and 0.8%, respectively.

In new production, intensive marketing of retail mortgages was a particular highlight during the period, doubling the number of approvals compared to the same period of the previous year, bringing the total to €10.53 billion, driven by MyHome, CaixaBank’s comprehensive ecosystem of home solutions. The bank’s market share of new mortgage production in Spain is now 23%.

In mortgage lending, the bank remains committed to fixed-rate loans, as they provide certainty to customers as to what they will be paying over the whole life of the loan. In the last seven years, 72% of residential mortgage lending has been originated at fixed rates and this figure has risen to over 90% in the first nine months of this year.

In consumer lending, new financing amounted to €7.68 billion between January and September 2022, up 23% on the same period of the previous year.

As for lending to businesses, new production in the first nine months of the year came to roughly €32 billion, up 47% year-on-year, thanks to a specialised model to accompany and support the industrial sector.

Management of customer funds

Total customer funds amounted to €612.5 billion, down 1.2% in the year, but up 1.8% excluding the market effect. Meanwhile, assets under management stood at €144.13 billion. The performance here (-8.8% in the year and -0.8% in the quarter) was largely due to high market volatility. Despite this, the bank was able to attract net inflows of €10.95 billion in the period. These figures make CaixaBank the leader when it comes to net inflows in mutual funds in the Spanish market, with growth in the market share for the main long-term savings products.

In addition, as part of its commitment to offering the best service and customer experience, CaixaBank has continued to expand its catalogue of new solutions this year. It has recently launched 'MyBox Retirement', a service where the customer sets their target capital for retirement and arranges a monthly savings plan to achieve it, combining liquidity and tax benefits with family protection.

Optimal risk management

The figures released today by CaixaBank display sound risk management, as evidenced by a further decline in the NPL ratio, which fell to 3% and is now at its lowest level since 2008. Non-performing loans fell to €11.64 billion, following an improvement in asset quality indicators and active management of NPLs, which have fallen by €1.99 billion in the year to date and by €782 million in the quarter. The cost of risk (trailing 12 months) remained suitably low at 0.23%.

Loan-loss provisions stood at €7.87 billion at the end of September and the NPL coverage ratio improved by five percentage points to reach 68%. During the year, lower loan-loss provisions were recorded (-11.1%) and other provisions also fell (-45.7%).

In view of the latent macroeconomic uncertainty, CaixaBank maintains a collective provision fund of €1.26 billion, which remained stable in the quarter.

As for loans partially guaranteed by the Official Credit Institute (ICO), 28% of the total has already been repaid or cancelled. Of the remaining amount, 95% are already repaying principal while just 4.4% is classified as non-performing.

Strong capital and liquidity position

Between January and September, CaixaBank maintained a strong position in terms of both capital and liquidity. The CET1 capital ratio is now 12.4% (12.1% without IFRS 9 transitional adjustments), following the extraordinary impact of the share buyback programme (-83 basis points, corresponding to the total deduction of the maximum authorised amount of €1.8 billion). In this context, the bank achieved organic capital generation of 92 basis points over the first nine months of the year.

Aside from its capital strength, the bank has a comfortable liquidity structure, with total liquid assets of €141.98 billion and a Liquidity Coverage Ratio (LCR) of 276%, well above the minimum regulatory requirement of 100%.

Financial strength to support customers and society

The financial strength shown by CaixaBank's results for the first nine months of the year allow the bank to deliver on its commitment of supporting its customers and society in general, which is part of the Group’s DNA.

Along these lines, CaixaBank has recently announced its new brand purpose: ‘Standing by people for everything that matters’, reaffirming its commitment to being close to society and all its stakeholders – starting with customers –, reinforcing its corporate culture, and aligning with its 2022–2024 Strategic Plan, which was unveiled in May.

The bank has decided to define a new brand purpose following the completion of the integration with Bankia, thus consolidating its status as the largest financial group in Spain. Following on from this, CaixaBank has also revisited its slogan, which is now "You and I. Together", showcasing its commitment to remain close to people and society as a whole, and to be part of their lives, their reality and their needs.

On a day-to-day basis, the bank pursues its social commitment by working towards financial inclusion through the most extensive network of branches and ATMs in Spain, among other endeavours. CaixaBank is present in more than 2,200 municipalities and maintains its commitment to not abandoning towns and villages. It is the only bank in 470 towns, while a further 626 have their banking needs covered by a mobile branch (the “ofimóvil” branch in a bus).

Moreover, it has launched specific solutions for more vulnerable segments of society: 357,000 customers now have a commission-free social account. In the last ten years, CaixaBank has signed 35% of the total contracts in the sector which abide by the Mortgage Code of Best Practices. Support to society is also reinforced through MicroBank, CaixaBank's social bank and the leader in Europe for microlending, through the work of CaixaBank Dualiza, driving employment and education, and through the corporate volunteering programme; among other initiatives.

Video CaixaBank's CEO, Gonzalo Gortazar

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}